By: Nicsa Digital Assets Committee

Nicsa's Digital Assets Committee continues to explore the technologies and market developments shaping the future of asset and wealth management. During our May committee meeting, members welcomed Tom Pikett, Executive Director, DTCC Digital Assets, for an engaging discussion on tokenization, market infrastructure, and the practical considerations surrounding institutional adoption of digital assets.

Tokenization Is an Evolution of Existing Markets

As interest in digital assets continues to grow, much of the industry's attention has shifted from cryptocurrency to the tokenization of traditional financial assets. Rather than creating entirely new securities, tokenization allows existing assets, including equities, exchange traded funds, and U.S. Treasuries, to be represented digitally while maintaining the same underlying ownership and regulatory framework.

Tom emphasized that this approach is less about reinventing financial markets and more about modernizing the infrastructure that supports them. By leveraging distributed ledger technology, firms have the opportunity to enhance operational efficiency while preserving the trust, governance, and protections that underpin today's markets.

Interoperability Will Shape the Future

One of the strongest themes throughout the discussion was interoperability. As additional blockchain networks and digital asset platforms emerge, the industry faces a growing challenge: ensuring tokenized assets can move efficiently across multiple environments without creating fragmented markets.

Tom shared DTCC's vision for supporting tokenized assets across multiple blockchain networks while maintaining consistent books and records. Rather than requiring firms to commit to a single blockchain, this approach is designed to provide greater flexibility as digital ecosystems continue to evolve.

Collateral Management Presents an Immediate Opportunity

While tokenization has many potential applications, collateral management emerged as one of the most compelling near-term use cases.

The discussion explored how tokenized assets may improve collateral mobility by enabling assets to move more efficiently, supporting automated workflows, and laying the groundwork for more dynamic collateral management. Participants also discussed the role of smart contracts and digital infrastructure in helping to streamline operational processes that have traditionally relied on manual intervention.

Innovation Requires Strong Governance

Technology alone will not drive institutional adoption.

Committee members engaged in a thoughtful discussion around governance, custody models, wallet management, regulatory oversight, and investor protections. Throughout the session, Tom reinforced that trusted market infrastructure remains essential as firms adopt new technologies. Maintaining accurate books and records, supporting compliance requirements, and preserving existing market safeguards are expected to remain important considerations as tokenization continues to mature.

Looking Ahead

As digital assets continue to evolve, industry collaboration remains essential. Conversations like these help bridge the gap between emerging technologies and real-world implementation, giving market participants the opportunity to better understand both the opportunities and operational considerations associated with tokenization.

Nicsa extends its sincere appreciation to Tom Pikett and DTCC for sharing their expertise with the Digital Assets Committee. We look forward to continuing these discussions as the digital asset landscape evolves.

To learn more about Nicsa's Digital Assets Committee or how to get involved, contact [email protected].

By: Nicsa Data Analytics Committee

Every financial organization has more data than ever, but the real advantage comes from knowing how to use it with purpose. What once felt like a specialized technical discipline has become an essential business capability for professionals across operations, compliance, client service, and investment teams. As markets move faster, regulatory expectations grow, and AI becomes part of everyday workflows, data analytics is no longer just about reporting what happened. It is about building the skills, judgment, and collaborative mindset needed to turn information into trusted decisions and meaningful innovation.

In today’s hyper-connected digital economy, data is often described as the new oil. A more accurate view is that it serves as a raw energy source that powers decision-making. Across financial services and asset servicing in particular, data is not abstract. It sits at the center of operations, supporting everything from compliance monitoring to investment strategy execution.

The data analytics journey moves from foundational skills

to trusted financial innovation.

For example, firms are using analytics to flag suspicious trading activity in near real time, reducing regulatory risk, while portfolio managers rely on data models to rebalance assets based on shifting market conditions. These are not future-state ideas, they are already embedded in daily workflows.

Defining Data Analytics in a Complex World

Data analytics goes far beyond charts and spreadsheets. It is the end-to-end process of examining raw data to uncover patterns, generate insights, and support informed decision-making. This includes data preparation, statistical analysis, and predictive modeling.

In financial services, this process transforms large volumes of data such as trade records, client information, market data, and regulatory inputs into actionable business intelligence. A common use case is client segmentation, where firms analyze behavior and transaction history to tailor products or outreach strategies. Another is operational efficiency, where analytics helps identify bottlenecks in trade processing or settlement cycles.

The Path to Upskilling: Building the Maker Mindset

As industries continue shifting toward AI-driven workflows, the demand for data skills has accelerated. Professionals increasingly need to move from passive consumers of data to active builders of analytical solutions.

Automation and Visualization Tools: Platforms like Alteryx and Power BI enable efficient data preparation, blending, and visualization, turning complex datasets into interactive insights. For instance, operations teams can automate reconciliation processes and surface exceptions through dashboards instead of manual reviews.

Programming Foundations: Python has become a core language in analytics due to its flexibility and strong ecosystem, supporting everything from automation to machine learning. A practical application is building scripts that pull and clean market data daily, feeding directly into risk models.

Continuous Learning: Online platforms such as Udemy provide accessible entry points for building both practical and theoretical knowledge. Many professionals apply these skills immediately, such as creating small forecasting models to support budgeting or scenario analysis.

The Role of Community and Collaboration

Technical skills alone are not enough. Progress in data analytics is often driven by shared knowledge and real-world application.

Industry groups, such as the Nicsa Data and Analytics Committee, help bridge theory and practice by enabling professionals to exchange insights, use cases, and challenges. These forums often surface practical applications, like how firms are standardizing ESG data reporting or using shared frameworks to improve data governance.

Collaboration also accelerates innovation. A solution developed for one use case, such as automating client reporting, can often be adapted across teams or even across organizations.

The Next Phase: From Insight to Foresight

As foundational skills mature, the focus shifts from understanding past performance to shaping future outcomes.

AI and Machine Learning: Enables predictive and prescriptive analytics to anticipate trends and guide decisions. For example, firms are using machine learning models to predict client churn or identify which accounts may require proactive engagement.

Generative AI in Workflows: Redefines how data is accessed and used, including automation and improved discovery. Analysts can now query complex datasets using natural language, significantly reducing the time required to generate insights.

Ethical AI and Data Governance: Ensures transparency, accountability, and trust in advanced analytics. This is especially critical in use cases like credit decisioning or fraud detection, where biased or opaque models can introduce risk.

The Path Forward: Resources and Ecosystems

The data analytics journey is continuous and supported by a growing ecosystem of tools and communities.

Industry engagement through groups like the Nicsa Data and Analytics Committee, where real-world applications and lessons learned are shared.

Advanced education platforms such as Coursera and edX, often used to build specialized skills like machine learning or data engineering.

Developer and research communities like GitHub, Stack Overflow, and arXiv, where practitioners collaborate and refine solutions.

Looking Ahead

The data analytics journey doesn't end with dashboards or reports. It continues as organizations turn insights into action and embrace new technologies that make better decisions possible.

The greatest value comes from combining strong data practices with curiosity, collaboration, and a willingness to adapt. As AI and predictive analytics become more accessible, organizations that build a solid foundation today will be best positioned to uncover new opportunities, solve complex challenges, and create lasting business value.

Continuing the Conversation

The Nicsa Data Analytics Committee will continue to explore these themes, with a focus on shared learning across members.

For those interested in contributing perspectives or participating in future discussions, we encourage you to join the conversation. For information about how to get involved in Nicsa’s Committees, reach out to i[email protected].

By: Nicsa Data Analytics Committee

Data continues to play an increasingly critical role across the asset and wealth management industry, influencing everything from business strategy and operational efficiency to client engagement and regulatory readiness. As organizations navigate evolving technologies, growing data demands, and new opportunities for innovation, understanding the industry's priorities has never been more important.

To help capture these insights, Nicsa's Data Analytics Committee is launching a brief industry survey designed to better understand the key challenges, opportunities, and strategic initiatives shaping organizations today.

Why Participate?

The survey will help the committee identify emerging trends, better understand member needs, and uncover areas where additional resources, education, and industry collaboration can provide value. Insights gathered will help inform future committee programming, thought leadership, and discussions that support the broader Nicsa community.

By sharing your perspective, you'll contribute to a more comprehensive view of how firms are leveraging data and analytics—and help guide conversations that drive meaningful industry progress.

Continuing the Conversation

The Nicsa Data Analytics Committee will continue to explore these themes, with a focus on shared learning across members.

For those interested in contributing perspectives or participating in future discussions, we encourage you to join the conversation. For information about how to get involved in Nicsa’s Committees, reach out to i[email protected].

By: Nicsa Technology & Innovation Committee

Recent survey results from the Nicsa Technology & Innovation Committee offer a directional view into how Committee members are thinking about digital assets—highlighting both areas of strong understanding and where questions are now shifting toward practical application.

A Closer Look at the Survey Results

While foundational concepts such as blockchain and tokenization are well understood, responses were more mixed in areas tied to implementation. This includes more specialized technical concepts on distributed ledger mechanics and the evolving US regulatory landscape, where recent guidance has sought to clarify how existing commodities and securities laws apply to various types of digital assets, and regulators continue to refine approaches through ongoing rulemaking efforts and industry engagement.

The Conversation Is Moving Toward Real-World Use

The survey showed what participants know and the discussion that followed revealed what they are thinking about next.

Rather than focusing on definitions, the conversation shifted toward how digital assets can be used:

Custody as an Operational Consideration

Survey responses indicated a general understanding that digital asset custody differs from traditional custody, particularly in relation to safeguarding private keys.

Participants discussed how this difference introduces new considerations—around governance, access, and operational processes—that extend beyond traditional custody models.

This reflects a broader theme: moving from understanding theoretical concepts to thinking through how they work in practice.

Continuing the Conversation

The Nicsa Technology & Innovation Committee will continue to explore these themes, with a focus on operational use and shared learning across members.

For those interested in contributing perspectives or participating in future discussions, we encourage you to join the conversation. For information about how to get involved in Nicsa’s Committee, reach out to i[email protected].

By: Nicsa Unclaimed Property Committee & Nicsa Retirement Committee

Collaboration is essential as regulatory expectations for unclaimed property continue to evolve across the asset and wealth management industry. Through a joint effort by NICSA’s Unclaimed Property Committee and Retirement Committee, members are aligning perspectives and navigating increasingly complex requirements across ERISA and non-ERISA frameworks. Central to this effort is the ERISA and Non-ERISA Unclaimed Property Reporting Guide, developed and presented by long-time NICSA member Abandoned Property Advisors (APA).

This work is particularly timely as policymakers consider proposals such as H.R. 5325, which could introduce new frameworks for handling unclaimed retirement distributions. While intended to improve participant outcomes, such proposals underscore the need to clearly distinguish between ERISA-governed plan assets and non-ERISA accounts. This contribution reflects the strength of member-led engagement—bringing practical insights, aligning industry perspectives, and helping firms interpret complex scenarios with greater confidence. The issues outlined in the guide underscore the importance of staying current as regulatory expectations evolve.

The guide focuses on key technical distinctions that firms must understand without overcomplicating execution. It differentiates between ERISA plan assets, which generally must remain within the plan trust and are subject to ongoing fiduciary obligations, and non-ERISA assets, such as IRAs, which are governed by state unclaimed property statutes and become reportable after the applicable dormancy periods.

It also addresses nuanced scenarios, including terminated plans pending PBGC transfer, post-distribution refunds, and accounts with returned mail or outdated participant information. Across these scenarios, the emphasis is on applying appropriate due diligence standards, leveraging regulatory guidance, and documenting fiduciary decisions to support compliance in an increasingly scrutinized environment.

As regulatory and legislative activity continues, firms must remain vigilant by increasing efforts to communicate with owners, update processes, monitor developments, and ensure consistency across operational and compliance functions.

Nicsa’s collaborative model brings these critical elements together, reinforcing the value of membership. By convening leaders from both the Unclaimed Property and Retirement Committees, Nicsa provides a forum for practical dialogue, peer exchange, and coordinated problem-solving.

Enhanced by contributions from member firms such as APA, these efforts help translate complex regulatory issues into actionable guidance. For firms evaluating their current practices, this industry collaboration—and access to experienced practitioners—can be an important part of maintaining alignment with evolving expectations.

Through its committees, Nicsa brings together diverse perspectives across the asset and wealth management industry to foster ongoing collaboration. To learn more about Nicsa membership or explore how your firm can participate in peer discussions, contact [email protected].

Observations contained in this work do not necessarily reflect the views of Nicsa or any member organization. Nothing herein is intended to be or should be construed as legal advice. Contact your own counsel in order to obtain advice regarding legal or regulatory matters.

By: Nicsa Data Analytics Committee

Nicsa's Data Analytics Committee, comprising executives in the asset and wealth management community, presents the following insights around AI Governance:

On the presupposition that computers, and by extension artificial intelligence, cannot be held accountable either morally or legally, business owners, AI engineers, and other AI actors in the financial services industry face the same question:

Who is responsible for AI failure?

And just as importantly, how do we implement AI while mitigating risk?

Why “Failure” Isn’t Hypothetical

Failure may sound extreme, but in the context of intellectual property disputes, data governance pressures, and geopolitical dependencies across infrastructure and supply chains, it is entirely plausible.

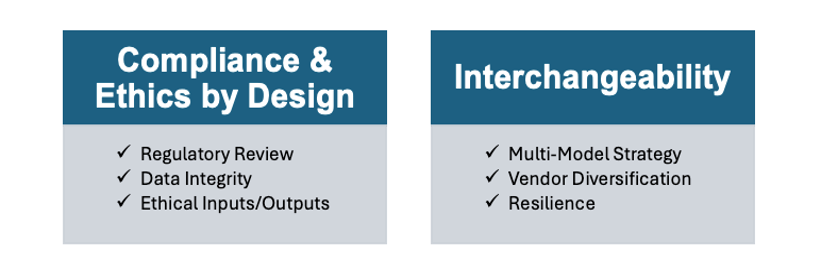

The question is not whether failure can occur, but whether organizations are equipped to absorb and manage it. This makes governance a core priority, not a downstream consideration. A practical AI Governance framework should be anchored by two principles: Compliance and Ethics by Design and Interchangeability.

A Simple Framework for AI Governance

1. Compliance and Ethics by Design

2. Interchangeability

Taking the lessons learned in a study which used “Adversarial Poetry1” (harmful requests reformulated in poetic form) to circumvent current safety mechanisms to utilize AI chatbots for the creation of content beyond its safety training protocol, we ought not to assume that current alignment methods and evaluation protocols are sufficient in defending against misuse. Independent consideration and review for regulatory (accounting for the possibility of stronger regulations in the future) and ethical compliance of AI models and platforms should be integrated into the onboarding process.

This consideration should include assessing risks related to the generation or replication of protected intellectual property, as well as the use of proprietary data in training and agent-driven workflows. It also requires deliberate oversight of both inputs and outputs, including how results are interpreted and applied. In this context, data quality and integrity are not just technical concerns, but core governance priorities that underpin reliable model performance and responsible business use.

Governance as Risk Management

Framing governance as a core element of risk management and business continuity expands the focus beyond inputs and outputs to include the models themselves and the providers behind them.

As AI adoption matures and scaling begins to plateau, a shift toward smaller, task-specific or locally deployed models offers clear advantages in resilience. Compared to reliance on large, generalized systems, these approaches reduce dependency risk and improve overall operational stability.

Where Governance Fits in Practice

At the enterprise level, diversifying across models and model families (AI models with shared origins and architecture), supported by infrastructure designed for interchangeability, enables more agile model selection within workflows. This approach reduces concentration risk as AI becomes embedded in critical operations and mitigates disruption from large-scale outages.

Closing Thought

While questions around AI risk remain, best practices will evolve with the technology. The immediate priority is clear: balance value and risk through disciplined governance. In the end, success will not be defined by how much AI is adopted, but by how well it is governed.

Looking Ahead

Nicsa’s Data Analytics Committee remains focused on fostering collaboration across executives in the asset and wealth industry. The Committee looks forward to continuing this dialogue in future meetings and encourages members to bring colleagues and new perspectives into the discussion. For information about how to get involved in Nicsa’s Committee, reach out to i[email protected].

By: Nicsa Fund Administration Committee

Nicsa’s Fund Administration Committee continues to serve as a forum for timely, practical discussions on the evolving challenges facing fund operations. At our latest meeting, members came together to explore one of the most complex areas in the industry today: private market valuations.

The session featured Liza Bowersox, Partner in Weaver’s Valuation Services practice, who led a thoughtful discussion on the realities of valuing private equity and venture capital investments.

Navigating Complexity in Private Markets

As private markets continue to grow and expand into new product structures, valuation practices are under increasing scrutiny. Liza highlighted several persistent challenges, including inconsistent financial reporting across portfolio companies and the difficulty of valuing early stage investments and complex instruments such as convertibles.

A key takeaway was the importance of strong governance. Clear separation of responsibilities between general partners, fund administrators, and third party valuation providers remains critical to maintaining independence and credibility in the valuation process.

The Case for Standardization and Discipline

One theme that resonated strongly with the group was the need for greater standardization. Establishing consistent information packages from portfolio companies can significantly improve the quality and reliability of valuations.

Liza also emphasized the role of backtesting as a best practice. Regularly comparing prior valuations against actual outcomes helps firms assess the effectiveness of their methodologies and identify areas for improvement.

Preparing for the Next Wave of Product Innovation

The conversation also touched on the continued expansion of registered products that include illiquid assets. While these structures are opening access to private markets, they also introduce new operational and regulatory considerations.

As noted during the discussion, these products will likely focus on less volatile investments and face heightened oversight from regulators. This puts additional pressure on firms to ensure their valuation frameworks are both robust and well documented.

Looking Ahead

The Fund Administration Committee remains focused on fostering collaboration across asset managers, service providers, and industry experts. As the landscape continues to evolve, these conversations are essential to helping firms stay ahead of emerging risks and opportunities.

Nicsa looks forward to continuing this dialogue in future meetings and encourages members to bring colleagues and new perspectives into the discussion. For information about how to get involved in the Committee, reach out to i[email protected].

In a recent global webinar, Inclusion in Finance (formerly the Diversity Project) introduced a transformative rebrand alongside an ambitious five-year strategy designed to accelerate inclusion, strengthen performance, and unify efforts across regions.

This is not a cosmetic change. It is a strategic evolution. Learn more by watching the replay: Watch the recording

A New Name, A Broader Mandate

After a decade of impact, the transition from the Diversity Project to Inclusion in Finance reflects maturity, momentum, and a stronger global alignment. Operating across three coordinated regions (UK, Europe, and North America), the organization remains locally responsive while increasingly aligned globally. This model ensures relevance across regulatory, cultural, and market-specific dynamics while amplifying collective impact.

The Business Case: Inclusion as a Performance Driver

A central theme of the webinar was the reframing of inclusion as a performance imperative, not a social initiative. New research on cognitive diversity highlights a compelling link between diverse thinking and investment outcomes. In the coming months, Inclusion in Finance will be developing tools to assess and harness diverse thinking.

The rebrand to Inclusion in Finance is more than a milestone—it is a platform for the next decade of progress in the asset and wealth management industry.

The message is clear: inclusion is not peripheral—it is foundational to performance, innovation, and long-term success.

For more information about Inclusion in Finance: Read the press release.

Nicsa’s $20,000 contribution underscores the collective impact of the asset and wealth management industry in driving meaningful change.

The power of industry collaboration was on full display at the 2026 SAMFund Soirée Boston, where Nicsa reinforced its commitment to purpose-driven leadership through its ongoing partnership with the Expect Miracles Foundation (EMF). Held on March 10, the event convened a passionate community dedicated to supporting young adult cancer survivors—an often underserved population navigating both health and financial challenges.

As part of this impactful evening, Sarah Walter of Nicsa presented a $20,000 check to EMF in support of its SAMFund Grant Program. This contribution represents the collective generosity of Nicsa’s global membership—firms across the asset and wealth management industry united by a shared mission to give back.

A Partnership Rooted in Purpose

Nicsa’s collaboration with EMF reflects a broader commitment to advancing social impact across the asset and wealth management industry. Through initiatives like Nicsa Gives Back, member firms channel their resources and influence to address critical needs beyond the financial ecosystem.

The SAMFund, a flagship program of EMF, provides direct financial assistance to young adult cancer survivors, helping them cover essential living expenses such as housing, transportation, and education. These grants play a pivotal role in enabling recipients to regain stability and pursue long-term goals.

Industry Leadership Beyond Markets

Nicsa’s $20,000 contribution is more than a donation—it is a reflection of the asset and wealth management industry’s growing role in driving social good. By aligning capital with compassion, Nicsa and its member firms continue to demonstrate that industry leadership extends beyond markets and into communities.

As the partnership with EMF evolves, Nicsa remains focused on expanding its impact, mobilizing its network, and supporting initiatives that deliver measurable outcomes for those in need.

With continued engagement from its members, Nicsa is well-positioned to deepen its contributions and amplify its role as a catalyst for change.

For more information on Nicsa Gives Back and its partnership with the Expect Miracles Foundation, visit: https://nicsa.org/nicsa-gives-back/

Authored by Sarah Walter, Head of Asset and Wealth Management Relationships at Nicsa

Private markets continue to play an increasingly central role in asset and wealth management strategies, driven by investor demand for differentiated return streams, income, and diversification. Nicsa’s Private Markets Committee convenes senior leaders from across asset management, wealth platforms, distribution, technology, and professional services to examine how firms are navigating this evolving landscape.

Formerly known as the Alternative Investments Committee, the group formally updated its name in 2025, with 95% of members voting in favor of the change. The new name, private markets, is more aligned with current industry terminology and better reflects the committee’s focus on private equity, private credit, real assets, and related structures.

Over the course of the past year, committee discussions consistently centered on practical implementation challenges rather than theoretical opportunity. Here are the key themes that guided the committee’s work in 2025 and will inform its priorities in 2026.

Expanding Access—Without Ignoring Constraints

Private market investments are reaching a broader audience, particularly through interval funds, tender offer funds, non-traded BDCs, non-traded REITs, and emerging use cases within defined contribution plans. Committee discussions highlighted growing interest in these structures, alongside sober recognition of the trade-offs they introduce.

Members spent considerable time examining how liquidity provisions, redemption mechanics, and portfolio construction considerations affect both sponsors and end investors. While access is expanding, firms remain highly disciplined in balancing product demand with operational feasibility and investor experience.

Liquidity, Structure, and Portfolio Fit

Liquidity management emerged as one of the committee’s most consistent topics. Discussions explored how intermittent liquidity vehicles can be incorporated into model portfolios, how rebalancing and prorating challenges are addressed, and where friction may still exist across platforms and custodians.

Committee members also examined how different fund structures—registered and unregistered—shape distribution strategy, compliance obligations, and investor suitability. Rather than seeking one-size-fits-all solutions, conversations emphasized the importance of aligning structure, liquidity, and use case.

Regulatory Guardrails Continue to Shape Design

Regulatory considerations remained front and center, particularly as firms evaluate private market exposure within registered vehicles and retirement plans. Committee discussions revisited ’40 Act limitations, distinctions between registered and private fund structures, and evolving regulatory expectations around illiquidity, disclosure, and investor protection.

Members noted that regulatory clarity—or lack thereof—continues to influence product design decisions, especially for firms seeking to scale private market offerings responsibly.

Technology as Infrastructure, Not Hype

Technology discussions throughout the year focused on solving friction, not chasing novelty. Committee members explored how platforms are streamlining onboarding, subscription processing, reporting, and data management for private market investments.

Emerging technologies such as tokenization and distributed ledger solutions were pragmatically discussed with current priorities lying in standardization, operational efficiency, and compliance-ready workflows. Platforms that reduce complexity—rather than introduce it—were viewed as critical enablers of growth.

Education as a Growth Enabler

Across meetings, committee members consistently pointed to education as a gating factor for broader adoption. Advisors and investors continue to grapple with complex structures, terminology, liquidity features, and tax considerations.

Discussions highlighted the need for clearer, compliance-approved educational materials and practical resources to support advisors, operations teams, and compliance professionals alike. As private markets become more accessible, the committee underscored that education must keep pace.

Looking Ahead

As private markets continue to evolve, the committee expects many of these themes to remain top of mind in 2026—particularly liquidity management, regulatory alignment, and scalable distribution models. The committee’s shift from “alternatives” to “private markets” reflects not just a naming update, but a broader maturation of the category itself.

Nicsa thanks the members of the Private Markets Committee and its guest speakers for their thoughtful contributions throughout the year. Their insights continue to inform meaningful dialogue across the asset and wealth management community.

To learn more about Nicsa’s committees or to get involved, visit nicsa.org.

Observations contained in this work do not necessarily reflect the views of Nicsa or any member organization. Nothing herein is intended to be or should be construed as legal advice. Firms should consult their own counsel regarding legal or regulatory matters.

Website Design By Branophia LLC